Sector context

More jobs and more diversity, record consents and a full pipeline, but prices are up and the sector faces workforce shortages and supply chain challenges.

On this page

Sector booming but feeling the headwinds

The building and construction sector is a significant contributor to New Zealand's economy. It contributed around 7% of total GDP in 20191 and employs over 10% of the national workforce2. The sector has continued to see a growth in employment numbers over the last year3, and, despite COVID-19 restrictions, has seen steady growth in business numbers.

MBIE's Sector Trends Annual Report 2021 found that the sector remained strong in the past year despite challenges faced as a result of the COVID-19 pandemic. Building consent numbers reached record-level highs and the workforce grew and gradually became more diverse, alongside a steady pipeline of domestic students and apprentices. The building landscape is also changing with the introduction of innovative building designs, technologies and materials.

Read MBIE's Construction Sector Trends report 2021 [PDF, 1.8 MB]

Despite this the sector is facing challenges, arising primarily from the COVID-19 pandemic. MBIE's September 2021 report on the pandemic and its impact on building system actors noted issues with:

- Rising costs of construction, in particular for products and freight

- Supply chain issues affecting both NZ-made and imported products

- Difficulty finding suitable staff to do the work.

Read MBIE's report on the pandemic and its impact on building system actors [PDF, 1 MB] — MBIE.govt.nz

"Capacity pressures remain very acute in the building sector, but building sector firms are finding it easier to pass on higher costs by raising prices."

NZIER Quarterly Survey of Business Opinion October 2021

More jobs, more women in those jobs, more diversity

Statistics indicate that the industry is becoming more diverse. In 2020 one-third of the construction workforce identified as being of the following ethnicities, an increase of 2% from 2018:

- Māori 15%

- Pacific 7%

- Asian 11%

The sector employed 291,800 people in the quarter ended September 2021, with 14.4% of these being female, up from 13.1% in September 2019 quarter5.

About 195,000 of the total number are in paid employment with the rest being classified as an employer, or as self-employed with no employees.

Full pipeline ahead

Government procurement is 20% of New Zealand construction and government can take a lead in setting procurement standards. According to MBIE'S National Construction Pipeline Report 2021, construction activity held up well against the COVID-19 pandemic and that is expected to continue.

Read MBIE's National Construction Pipeline Report 2021(external link) — MBIE.govt.nz

Total construction value fell by 5.7% in 2020 to $42.6bn and for 2021 MBIE forecasts it will grow to about $48.3bn in 2024, driven by the continued strength of the residential sector. Residential buildings contributed 58% of total construction value in 2020.

There are 2,588 projects currently in the New Zealand Infrastructure Commission, Te Waihanga pipeline, valued at over $64 billion. These are primarily sourced from government, councils and utility services The Pipeline includes projects that have a level of certainty around timing and includes projects from 159 organisations.

Pipeline(external link) — New Zealand Infrastructure Commission Te Waihanga

$29 billion worth of government projects are in the early planning or planning stage, suggesting a healthy longer-term pipeline of work. $24 billion worth of projects in the pipeline are under construction including a number of ‘shovel-ready’ infrastructure projects.

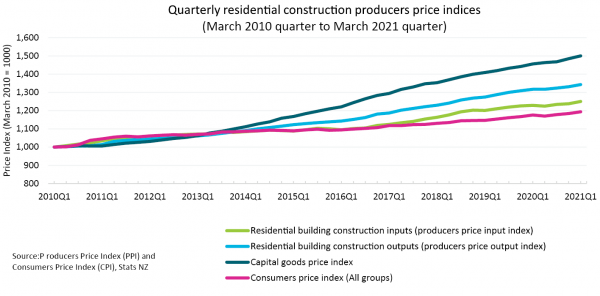

Building consents up 26%

There were 47,715 new dwellings consented in the year to October 2021, up 26% from 37,981 in the previous year to October.

Source: Building consents, Stats New Zealand.

Source: Stats New Zealand.

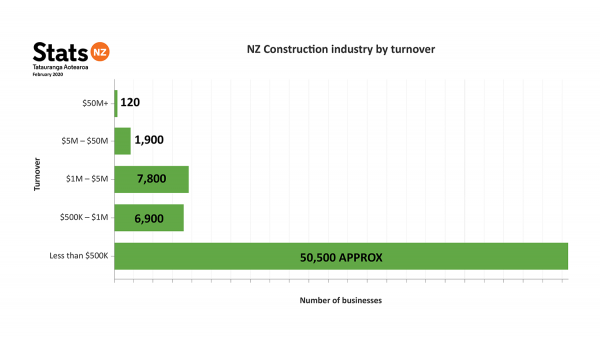

Small and very small businesses dominate

The sector remains dominated by small turnover businesses with low headcount.

Source: Stats New Zealand.

NZ Construction Industry by staff numbers

Source: BCITO, Master Builders.

Footnotes

1Stats NZ. Infoshare. GDP(P), Nominal, Actual, ANZSIC06 industry groups (external link)

2Stats NZ Household labour force survey: September 2021 quarter (Table 9)

3Stats NZ Household labour force survey: September 2021 quarter (Table 9)

4Building and Construction Sector Trends − Annual Report 2021 (mbie.govt.nz)

5Household labour force survey: September 2021 quarter (Table 9)